The ride hailing service, Lyft, is debuting on the Nadsaq on Friday and the multi-billion dollar question remains: is it cheap or expensive?

The answer to that question depends on who you talk to.

But before we dive into the analysis and the numbers that analysts are talking about…let’s appreciate the new category that Lyft itself is ringing in.

Initial public offerings are one of the more exciting vehicles associated with the stock market. They are the shiny, new object. An IPO starts from scratch with no history, no levels of support or resistance and with price discovery in full effect.

And then when you throw in a completely new category, Transportation as a Service (or TAAS), that’s where more divergence in opinion are in play.

The last time a new category was ushered into Wall Street via an IPO was the cannabis craze brought from Tilray Inc (TLRY) in the summer of 2018. Cannabis was nothing new…but with a high profile IPO, it brought a new conversation.

Nothing short of hysteria, including a massive short squeeze, ensued as Tilray (TLRY) (which priced 9.0mm shares at $17.00) hit a high of $300 in mid-September. That’s a wild 1664.7% gain if you top-ticked!

Now there is no way to expect that type of “March Madness” when it comes to the Lyft IPO — but it will still be exciting.

In one camp, Lyft is losing gobs of money and net profitability is no where in sight. “It takes a long time to dig yourself out of a $1 billion hole,” said Nicholas Colas, co-founder of DataTrek Research in the above-mentioned CNN article.

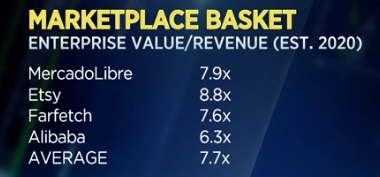

In another camp, Lyft is addressing a potentially $500billion-size market as one-of-two major players.  The revenue, an impressive $1billion in 2017, more than doubled in 2018. And while there are no true comps for Lyft, analysts on the roadshow are trying to digest forward looking numbers by comparing EV/Revenue to other high-flyers. (h/t CNBC). If you don’t want to click the link, Lyft is considered cheap versus the five featured in the CNBC photo.

The revenue, an impressive $1billion in 2017, more than doubled in 2018. And while there are no true comps for Lyft, analysts on the roadshow are trying to digest forward looking numbers by comparing EV/Revenue to other high-flyers. (h/t CNBC). If you don’t want to click the link, Lyft is considered cheap versus the five featured in the CNBC photo.

When it comes to IPO Boutique and our value to the syndicate player — we do not neccesarily care where Lyft trades in 2020. We serve our clients to pass information about subscription levels and price guidance and then give our opinion on if an IPO is worthy of a BUY at the issue price.

Our success directly correlates to if the new issue opens above the offering price.

When the long term outlook of a company is murky, with an inflated private valuation, is where it gets tricky in the short term.

Are large investors willing to “sit out the IPO” if their valuation of a company is currently lower than $19.6bn-$21.5bn at the $62-$68 range? If the book is full of retail accounts with a “fast money” attitude…what will be the effect on the stock price on day one.? If the stock heads south on day one — how many folks are ready to buy and hold knowing all the ammunition that investors in the “bear camp” have? What would be the floor for Lyft?

These are all risk that we (IPO Boutique) are all too familiar with given our 40-year history around the niche IPO sector of the stock market. If you have the accounts set up where you can participate in Lyft at the issue price (or any IPO)…rely on us to give you the full picture of the health of a deal prior to putting in your indication.

To circle back with our original question: Is the Lyft IPO cheap or expensive?

We like to rely on datapoints coming from the roadshow and follow the money to determine if day one will be a rosy outcome…or a red one.